Operating expenses in the second quarter were $6.24 per BOE compared to $4.20 per BOE in the second quarter of 2016, predominantly due to higher water handling costs and the use of temporary production equipment.

Greed meet Risk

The recent stock price drop in Seven Generations reminds us that valuation matters and even the most popular stocks can have a reassessment by the market as to what they perceive the value of the stock is. First let’s have a look at the recent market action and the press release that triggered the 18% drop in the stock price.

Seven Generations Stock Chart, courtesy Stockcharts.com

As you can see the price had been moving downwards to the right with the general market repricing of the Canadian Oil and Gas stocks in general. On August 3rd with the release of the latest quarterly results the company announced.

The rest of the press release is on the Seven Generations website, but generally good news on their growth initiatives was announced.

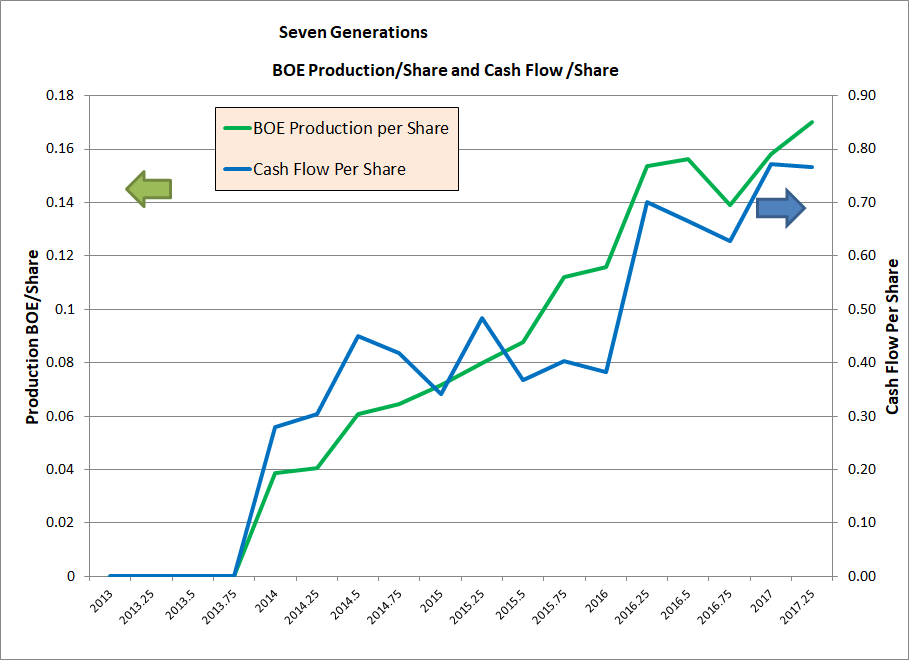

Production and Cash Flow per Share

While this by itself should not have caused any concern the stock dropped by 18 %, recovered slightly and more recently dropped some more. Since this is known to be a growth stock why don’t we have a look at the growth of the production and cash flow, to determine if the quarterly results showed a repricing due to lack of growth.

Seven Generations Production per share and Cash flow per share

There is nothing unusual or bad about the growth in production per share or growth in cash flow per share, upwards to the right just like what I would want in a growth stock. The most recent quarter showed continued growth in production per share, while cash flow per share was flat. This is perhaps one of the market indicators that caused investors some pause.

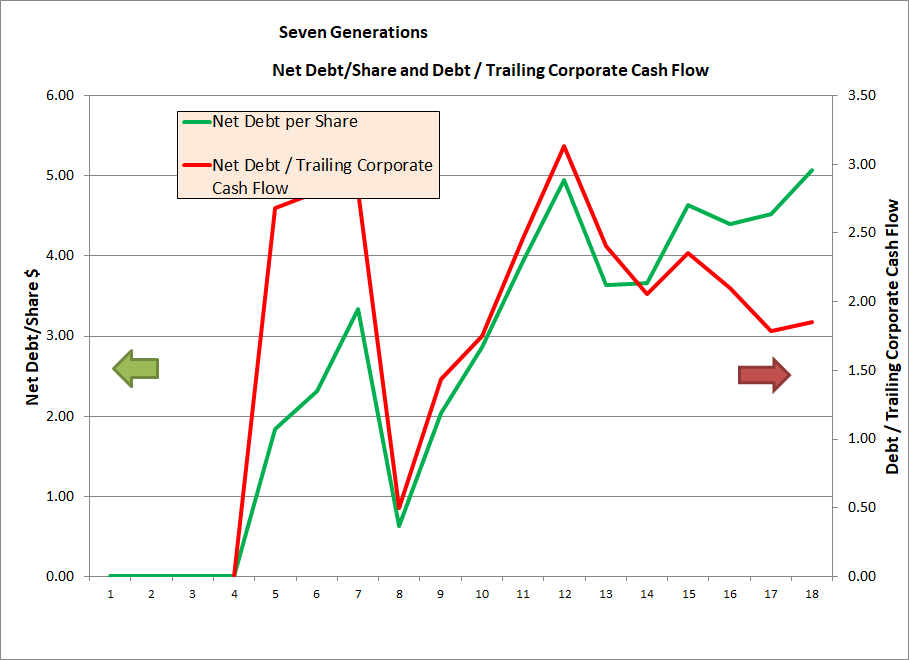

Debt Divided by Cash Flow and per Share

Debt is one of the metrics of oil companies fundamentals that has undone many companies this past down turn(ie Pennwest, Paramount, Twin Butte to name a few) so it is important to have a look at the debt to see if this is what upset investors.

Seven Generations Debt to Cash Flow

The graph indicates a prudent management team that is borrowing more to finance growth, but keeping the debt/cash flow below 2.0. There is no problem with debt as far as this graph can illustrate.

Valuation

The most important metric to keep focused on, in my opinion, is the valuation of the stock. A stock that is overpriced will drop severely with small changes in other fundamental measures as the growth gets repriced. Also the law of large numbers will also eventually catch up to the smaller growth oil and gas producers. As the company’s production gets larger, it becomes more difficult to grow at high percentage values. With lower growth the market will revalue the shares based on overvaluation in comparison to the growth rate.

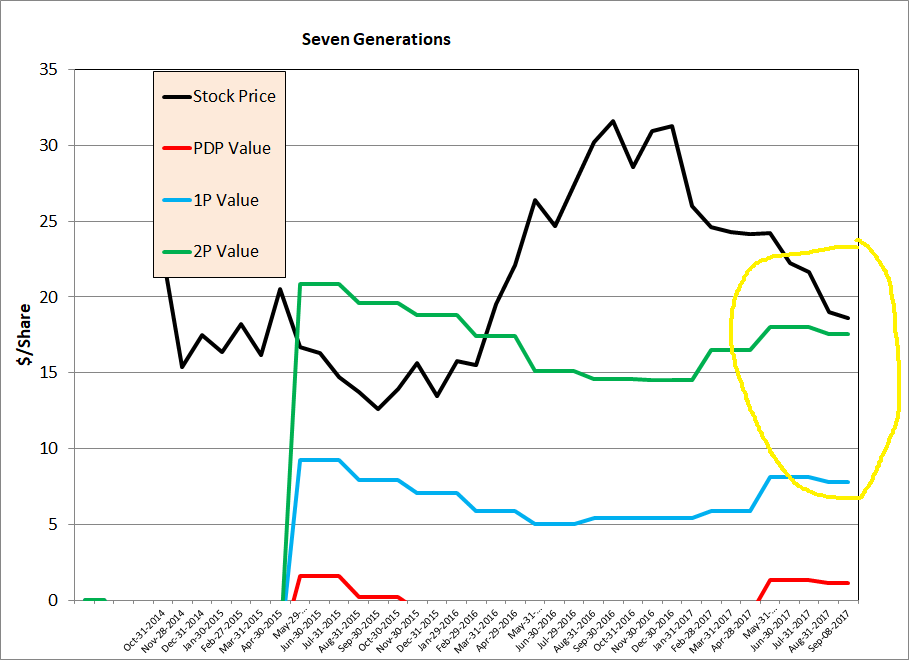

Seven Generation Valuation

This chart tells most of the story on why the stock dropped in price. With a press release talking to higher operating costs and production from the Seven Generation’s wells possibly showing more water production than normal, investors rethought the growth story. I can almost imagine some institutional money manager moving from having to own this stock at all costs, to finding a way to limit their losses. Greed meets risk, the risk being that investors will stop overpaying for growth and move their money elsewhere. The stock rocketed upward during 2016 to unrealistic levels and now has come down to only slightly over valued.

Seven Generations is growing their production at approximately 12% per year, per share(per share metrics are the only one that matters) which is close to their theoretical growth rate of 9% per year(On some future post I will have to explain some of the metrics I look at, such as theoretical growth). If they grow their $5.60/share PDP(producing wells) value at 12% per year for just over 10 years they will reach their present trading price of $18.5/share even after the drop. This is still a premium priced stock.(this does not include debt, including debt their pdp value is only $0.55/share)

I like this company, just the stock is not attractive at this price. I would rather own Yangarra with a growth rate of 90 % and trading below their 1P(total proved) reserve value. If small caps are not what you want then pick another larger stock from the Data Table on this website.

As always I won’t advise you on what you should do with your portfolio and you shouldn’t take this blog as a recommendation to buy or sell any security. Please consult with a qualified financial advisor before you buy or sell any security.

I see you like yangarra as well. I have seen this stock mentioned a couple of times on bnn. You read my mind

It was overhyped at the top, everyone was telling me to buy. I was going to buy some after it dropped, maybe now I’ll wait a bit.